All Categories

Featured

Table of Contents

- – What is included in Indexed Universal Life Int...

- – Who has the best customer service for Indexed ...

- – What is the best Indexed Universal Life Inter...

- – Why is Indexed Universal Life Plans important?

- – Who offers flexible Tax-advantaged Iul plans?

- – How do I apply for Flexible Premium Indexed ...

Indexed Universal Life (IUL) insurance is a sort of long-term life insurance policy plan that incorporates the features of standard universal life insurance coverage with the possibility for cash money value growth connected to the performance of a supply market index, such as the S&P 500 (High cash value IUL). Like other forms of long-term life insurance policy, IUL provides a survivor benefit that pays to the recipients when the insured dies

Cash money worth accumulation: A part of the premium settlements enters into a money value account, which makes passion with time. This money worth can be accessed or borrowed versus throughout the policyholder's life time. Indexing choice: IUL plans use the chance for cash money value growth based upon the performance of a stock exchange index.

What is included in Indexed Universal Life Interest Crediting coverage?

Similar to all life insurance coverage products, there is also a set of threats that insurance holders need to recognize prior to considering this kind of policy: Market threat: Among the primary dangers connected with IUL is market danger. Considering that the money value growth is linked to the efficiency of a securities market index, if the index carries out improperly, the money value might not grow as expected.

Enough liquidity: Insurance policy holders must have a secure economic scenario and be comfortable with the exceptional repayment demands of the IUL policy. IUL enables versatile premium payments within particular limits, yet it's vital to maintain the policy to ensure it achieves its intended goals. Interest in life insurance policy protection: People who need life insurance protection and a passion in money value development may find IUL appealing.

Prospects for IUL should have the ability to recognize the auto mechanics of the plan. IUL might not be the very best choice for individuals with a high tolerance for market risk, those that prioritize low-cost financial investments, or those with more instant monetary needs. Consulting with a certified economic expert that can supply customized assistance is vital prior to considering an IUL policy.

All registrants will certainly obtain a calendar invitation and web link to join the webinar via Zoom. Can not make it live? Register anyway and we'll send you a recording of the discussion the next day.

Who has the best customer service for Indexed Universal Life Premium Options?

You can underpay or skip costs, plus you may be able to readjust your fatality advantage.

Money worth, along with prospective growth of that worth via an equity index account. An option to allot component of the cash worth to a fixed interest choice.

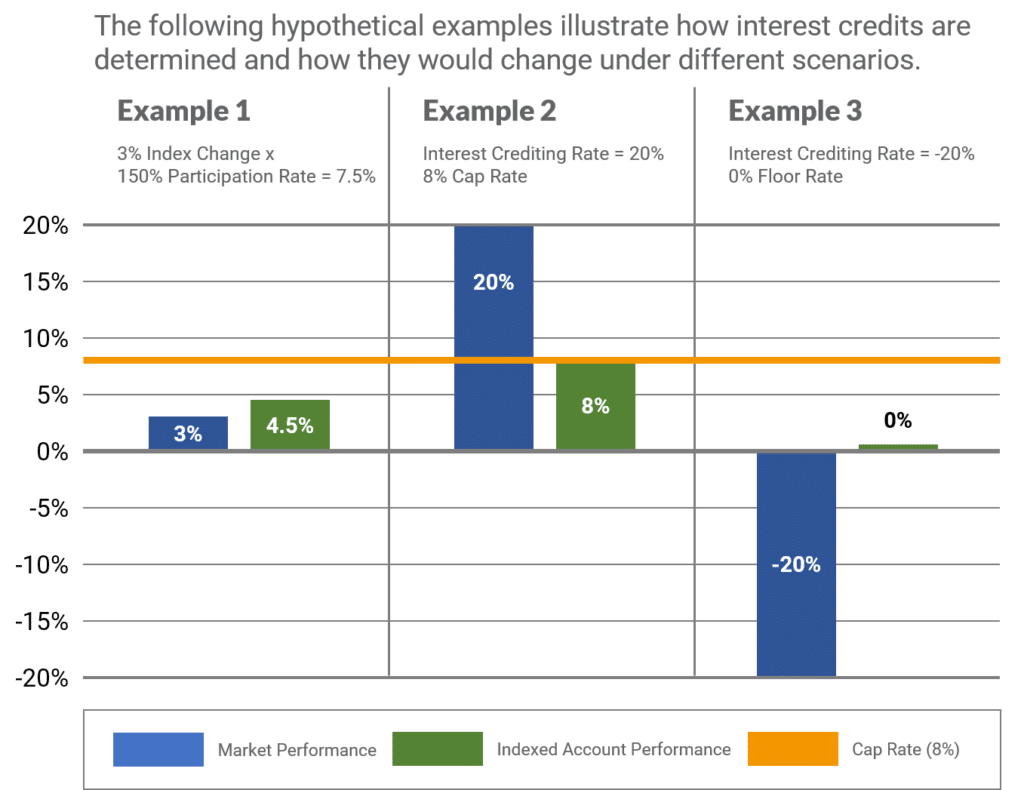

Insurance policy holders can decide the percentage allocated to the fixed and indexed accounts. The value of the selected index is taped at the start of the month and compared with the worth at the end of the month. If the index enhances during the month, passion is added to the cash worth.

The resulting interest is added to the cash worth. Some policies compute the index obtains as the amount of the modifications for the period, while other plans take an average of the day-to-day gains for a month.

What is the best Indexed Universal Life Interest Crediting option?

The price is set by the insurance provider and can be anywhere from 25% to even more than 100%. (The insurance firm can additionally change the participate price over the lifetime of the plan.) As an example, if the gain is 6%, the participation rate is 50%, and the current cash money value overall is $10,000, $300 is added to the money worth (6% x 50% x $10,000 = $300).

There are a number of advantages and disadvantages to consider before purchasing an IUL policy.: Just like common universal life insurance policy, the policyholder can increase their premiums or lower them in times of hardship.: Amounts credited to the money worth expand tax-deferred. The money worth can pay the insurance coverage premiums, permitting the insurance holder to lower or quit making out-of-pocket premium repayments.

Why is Indexed Universal Life Plans important?

Lots of IUL policies have a later maturity date than various other kinds of global life plans, with some ending when the insured reaches age 121 or even more. If the insured is still alive at that time, policies pay the survivor benefit (however not typically the money worth) and the earnings might be taxable.

: Smaller policy stated value do not use much benefit over regular UL insurance policies.: If the index drops, no rate of interest is attributed to the cash money worth. (Some policies provide a low assured price over a longer period.) Other financial investment vehicles use market indexes as a criteria for efficiency.

With IUL, the goal is to make money from upward motions in the index.: Since the insurance coverage firm just purchases alternatives in an index, you're not straight purchased stocks, so you don't profit when firms pay dividends to shareholders.: Insurers cost fees for managing your cash, which can drain cash money worth.

Who offers flexible Tax-advantaged Iul plans?

For a lot of individuals, no, IUL isn't far better than a 401(k) - IUL companies in terms of saving for retirement. A lot of IULs are best for high-net-worth individuals looking for methods to lower their taxed earnings or those that have maxed out their various other retirement alternatives. For everyone else, a 401(k) is a much better financial investment automobile since it does not carry the high charges and premiums of an IUL, plus there is no cap on the amount you may gain (unlike with an IUL policy)

, the revenues on your IUL will not be as high as a normal financial investment account. The high expense of costs and charges makes IULs costly and significantly much less cost effective than term life.

Indexed global life (IUL) insurance policy provides cash money worth plus a survivor benefit. The cash in the cash money worth account can gain passion with tracking an equity index, and with some commonly alloted to a fixed-rate account. Indexed global life plans cap how much money you can collect (often at less than 100%) and they are based on a perhaps volatile equity index.

How do I apply for Flexible Premium Indexed Universal Life?

A 401(k) is a far better choice for that function because it does not lug the high charges and premiums of an IUL policy, plus there is no cap on the quantity you may earn when spent. A lot of IUL plans are best for high-net-worth individuals looking for to lower their taxable income. Investopedia does not give tax obligation, investment, or economic services and advice.

If you're taking into consideration buying an indexed global life plan, first talk to a monetary advisor who can discuss the nuances and provide you an accurate image of the real capacity of an IUL plan. Make certain you comprehend exactly how the insurance firm will compute your rate of interest, revenues cap, and fees that could be evaluated.

{kind=link}

Table of Contents

- – What is included in Indexed Universal Life Int...

- – Who has the best customer service for Indexed ...

- – What is the best Indexed Universal Life Inter...

- – Why is Indexed Universal Life Plans important?

- – Who offers flexible Tax-advantaged Iul plans?

- – How do I apply for Flexible Premium Indexed ...

Latest Posts

Flexible Premium Indexed Adjustable Life Insurance

Life Insurance Term Vs Universal

Iul University

More

Latest Posts

Flexible Premium Indexed Adjustable Life Insurance

Life Insurance Term Vs Universal

Iul University